YANGON—While joint-venture proposals from foreign insurance companies are being reviewed by the country’s insurance business regulatory board, some of Myanmar’s largest insurance companies are already building bridges to leverage foreign expertise for the growth of Myanmar’s nascent insurance industry.

After two years of delays, Myanmar began allowing insurance companies to operate in the country’s life insurance market for the first time in April. The Ministry of Planning and Finance—which oversees the regulatory board—has granted licenses to five foreign companies thus far: Chubb Tempest Reinsurance of the United States; Dai Ichi Life Insurance of Japan; AIA of Hong Kong; Prudential of England; and Manufacturers Life Insurance of Canada.

At a press event held by IKBZ at Burma Bistro this week, IKBZ Deputy Managing Director Anil Mancham said the company is “in advanced discussions with a Japanese company” that will have a minority stake in the company once the joint venture is approved.

That company—Mitsui Sumitomo Insurance Co. Ltd. (MSIG)—already has some experience in Myanmar; it is one of only three Japanese companies granted permission to operate non-life insurance businesses in the Thilawa Special Economic Zone, on Yangon’s outskirts, along with Tokio Marine & Nichido Fire Insurance and Sampo Japan Insurance.

MSIG is one of Japan’s largest insurance operators, with operations in several international markets, including many in Southeast Asia.

“We are very supportive of the market opening to foreign companies. We believe growth will be accelerated by foreign players bringing their talent, expertise and industry international best practices,” Mancham told The Irrawaddy. “We see it as a win-win situation,” he said. While domestic growth has been strong, foreign partnerships “mean we’ll gain access to international best practices.”

IKBZ Vice Chairman U Nyo Myint largely agreed.

“We need to build personal capital, we need technology transfers, exposure and networking—those are the four main things we need from international partners,” he said. “We benefit from international investors. We don’t need [financial] capital, we need experience and technology.”

According to U Zaw Naing, the regulatory board’s secretary, companies can obtain up to a 35-percent stake in joint insurance ventures while the remaining 65 percent must be locally owned.

Six more foreign companies have submitted joint-venture proposals to do business in Myanmar. U Zaw Naing declined to disclose the names of the companies to The Irrawaddy earlier this week but said the proposals would likely be approved by next month.

U Myo Min Thu, executive director of AYA Myanmar Insurance—which is also partnering with a Japanese company—previously told The Irrawaddy, “Local companies will grow bigger due to the investment of foreign companies. This will create job opportunities and contribute to the national economy.”

Insurance in Myanmar

The Burma Bistro event was held to announce the findings of an internal IKBZ study on the present and future insurance market in Myanmar.

“We did this survey to know more about our customers—what are their concerns, what are their views on the financial sector, what insurance products do they know about,” U Nyo Myint explained.

The survey included 1,000 respondents from seven states across the country and found that just 17 percent of respondents were familiar with the concept of insurance. Of that 17 percent, however, 60 percent expressed interest in purchasing insurance products, mostly life.

Currently, there are 19 local companies providing general and life insurance in Myanmar.

“Our number one priority is having enough people on the ground to educate Myanmar consumers,” Mancham said. “We need to offer insurance awareness to Myanmar citizens.”

Seventy percent of survey respondents lived in urban areas and 30 percent lived in rural areas. Respondents were evenly split between men and women and distributed by age to reflect the country’s demographics.

Karma points

Interestingly, 22 percent of respondents cited beliefs and attitudes surrounding karma as the main factor keeping them from buying insurance. Or, as Mancham put it, “Many respondents believe in karma, and not insurance.”

“Some would rather give money to a monk or a charity” as their own form of insurance, said Marc Bakker, head of marketing and communications for IKBZ. Alternatively, mitigating unforeseen disaster is also sometimes seen as an attempt at cheating fate—like trying to escape a rightful punishment for the sins of a past life.

“But [insurance] isn’t about protecting yourself, it’s about protecting your loved ones,” Bakker said. “Just because you did something in a past life doesn’t mean they have to pay for it in this one.”

It may not be so hard of a sell, with the overwhelming majority of interested survey respondents citing the protection and betterment of the lives of their family members as the primary motivating factor driving their interest.

“In Myanmar the focus on the family is clear and takes precedence over self,” a report based on the survey states.

Thirty-three percent of respondents said they believed insurance products are just too complicated to engage with. While this split is bigger in rural and urban populations, those two groups responded remarkably similar to most survey questions.

“The difference between the urban and the rural is a lot smaller than you’d expect. Priority-wise, they’re almost identical—family, education, et cetera,” Bakker said.

“Developing this [market] can support Myanmar’s economic development and individual welfare,” said Vicky Bowman, director of the Myanmar Centre for Responsible Business, which encourages responsible business practices in Myanmar with a focus on human rights. She called the retail insurance market for individuals mostly low risk.

“The main responsible business challenge for foreign investors in the insurance market in Myanmar, as for most service sectors, such as estate agents and the banking sector, is likely to be ‘know your customer (KYC)’ risk,” she said, a practice more important for corporate insurance.

About to boom

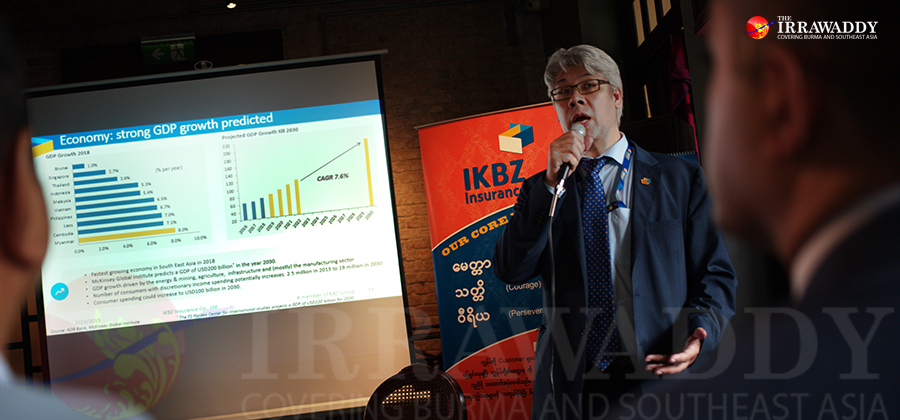

The contribution insurance markets make to national GDPs varies widely among countries and regions. For most Southeast Asian nations, insurance constitutes between 3 and 8 percent of total GDP.

Insurance premiums currently contribute just .8 percent to Myanmar’s GDP.

IKBZ projections suggest that could increase to 1.5 percent over the next year, making it a 1.75-trillion-kyat market.

With Myanmar’s general rate of GDP growth among the highest in the region, at 8 percent annually, those numbers could become significantly larger in the near-future.

“In the next 10 years, Myanmar’s insurance sector could double or triple in size as we get closer to the regional averages,” Bakker said. “We are seeing a growth in average family incomes, in the size of the middle class—all of which makes insurance more affordable as time goes by.”

Myanmar’s current GDP is less than $70 billion, according to the World Bank. Estimates from the Asian Development Bank and the McKinsey Global Institute suggest that number will reach $US200 billion by 2030.

“The Myanmar insurance market is primed to take off,” Bakker said.

You may also like these stories:

Local, Foreign Insurance Cos. Readying to Sell in Myanmar

5 Foreign Firms Licensed to Enter Myanmar’s Fledgling Life Insurance Market

Myanmar Opens Up to Foreign Insurance Companies

{kind=link}